CHILD EDUCATION PLANNER

Are you investing enough for your child's higher education?

Smart Planning Tool

What Is a Child Education Planning Calculator

How Does ICICI Pru Life Child Education Planner Works?

-

The calculator also offers insights on how much you need to invest monthly, half-yearly or annually and for how long to achieve your goal.

The calculator also offers insights on how much you need to invest monthly, half-yearly or annually and for how long to achieve your goal. -

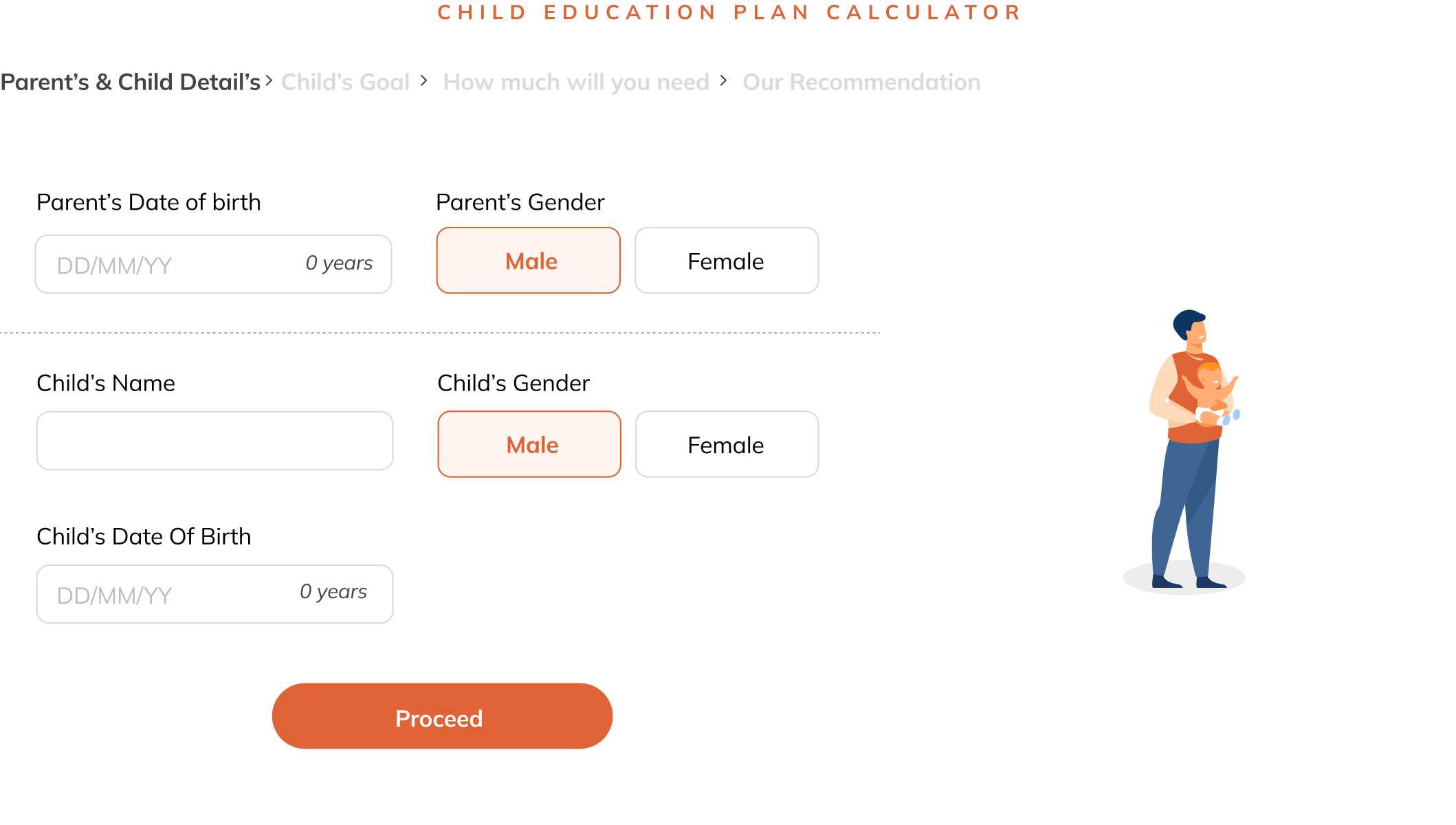

The child education calculator works by taking inputs such as:

Parent's date of birthParent's genderChild's nameChild's genderChild's date of birth

Parent's date of birthParent's genderChild's nameChild's genderChild's date of birth -

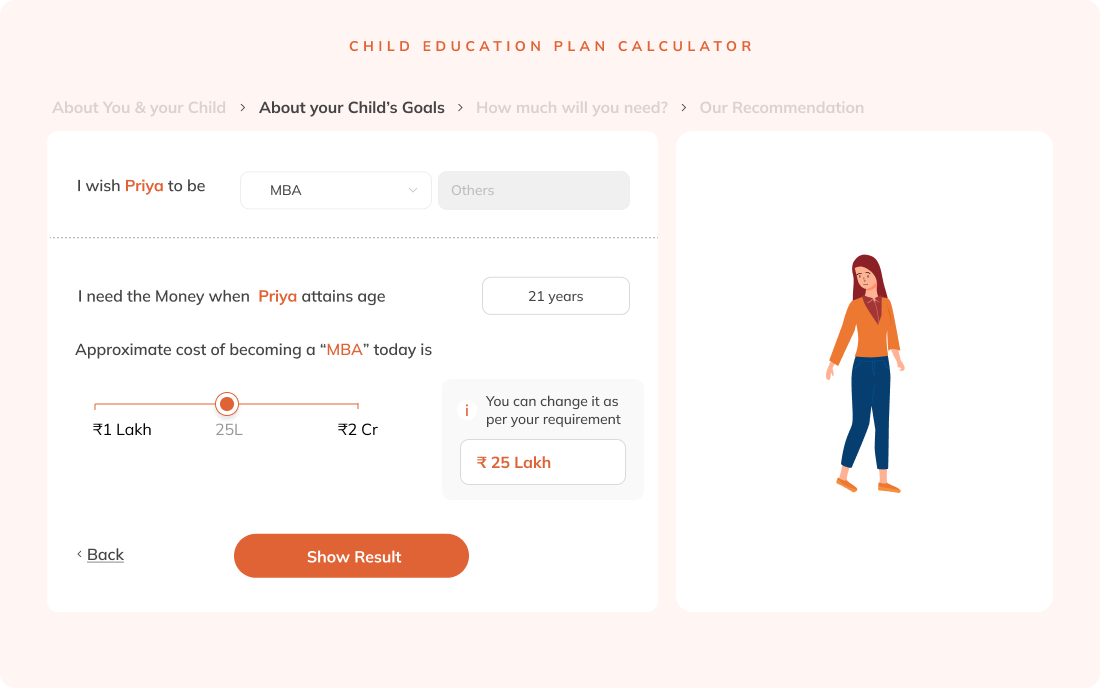

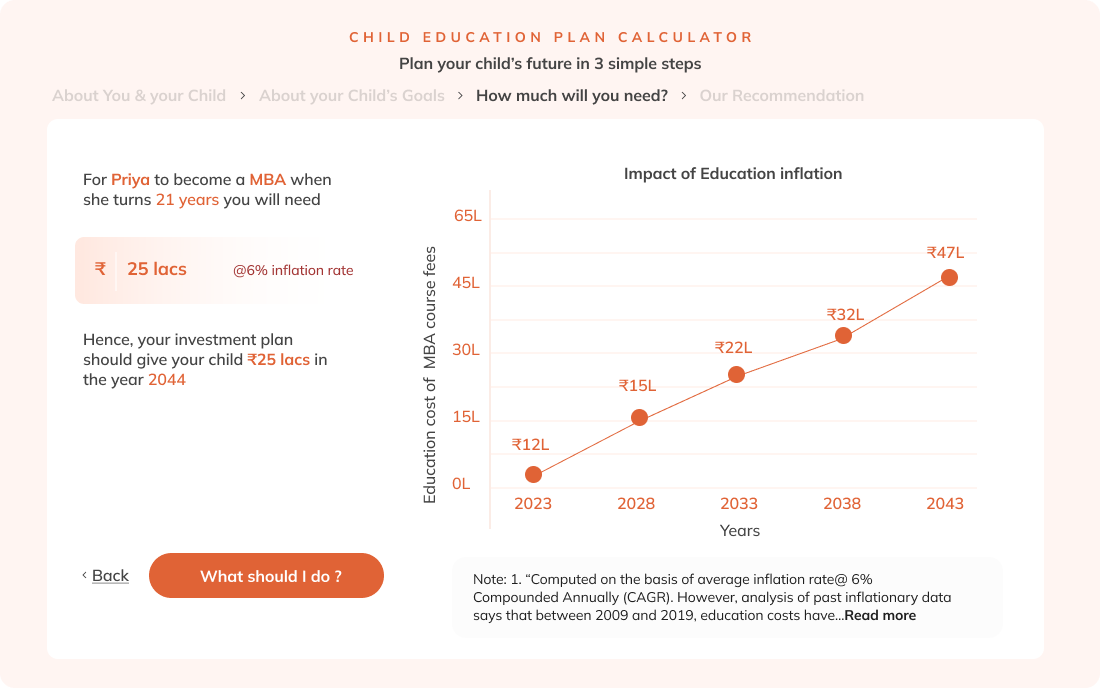

It then factors in the career or profession your child aims to pursue and the age at which they will need the funds. Based on these details, the calculator shows you the current average cost of education for that profession and how education inflation will impact this cost over time.

It then factors in the career or profession your child aims to pursue and the age at which they will need the funds. Based on these details, the calculator shows you the current average cost of education for that profession and how education inflation will impact this cost over time. -

Once you know the future savings estimate for your child's education needs, you can plan efficiently.

Once you know the future savings estimate for your child's education needs, you can plan efficiently. -

The calculator also offers insights on how much you need to invest monthly, half-yearly or annually and for how long to achieve your goal.

-

The child education calculator works by taking inputs such as:

Parent's date of birthParent's genderChild's nameChild's genderChild's date of birth

Quick Guide

How to use a child plan calculator: Step-by-step guide

What Are the Advantages of Using a Child Education Planning Calculator?

-

Risk Mitigation:

This calculator helps reduce financial risk by giving you a clear picture of your future needs. It allows you to make more calculated investment decisions that are better aligned with your goals. This minimises the chances of falling short when the time comes. -

Provides a roadmap:

A child education planner acts as a plan of action. It gives you an indication of the amount of fund required to fulfil your child's aspirations. A lot of people procrastinate because they are unaware of how much money they will need in the future. But, with this child education calculator, you will get a sense of the funds required and start planning immediately. -

Offers an estimate:

The child education plan premium calculator helps you evaluate how much you need to save to reach your desired goal. Every child is unique and may have different dreams. However, as a parent, you need to be prepared for any and everything. The calculator lets you plan and save for distinct purposes, such as education in top universities, education overseas, professional courses etc. -

Let's you compare:

A child education plan calculator in India can be used to compare the returns of different products available in the country. You can also compare the modes and frequencies of investment. This helps you make an informed decision and streamline your finances properly. -

Helps in tracking your goals:

Using a child education planner can also be helpful in other cases. The planner lets you monitor your goal and progress. It helps you understand where you stand and how much more you need to save. In the case of an emergency, if you withdraw funds prematurely from the plan, the planner can help you understand the shortfall you need to make up for. -

Investment Insights:

The child education planning calculator offers investment insights to help you plan ahead. It highlights the expected rate of inflation and shows how it can impact your savings. This allows you to choose investments that aim to deliver returns higher than inflation. The calculator also suggests next steps and estimates how much you need to invest regularly to reach your goal. -

Risk Mitigation:

This calculator helps reduce financial risk by giving you a clear picture of your future needs. It allows you to make more calculated investment decisions that are better aligned with your goals. This minimises the chances of falling short when the time comes. -

Provides a roadmap:

A child education planner acts as a plan of action. It gives you an indication of the amount of fund required to fulfil your child's aspirations. A lot of people procrastinate because they are unaware of how much money they will need in the future. But, with this child education calculator, you will get a sense of the funds required and start planning immediately.

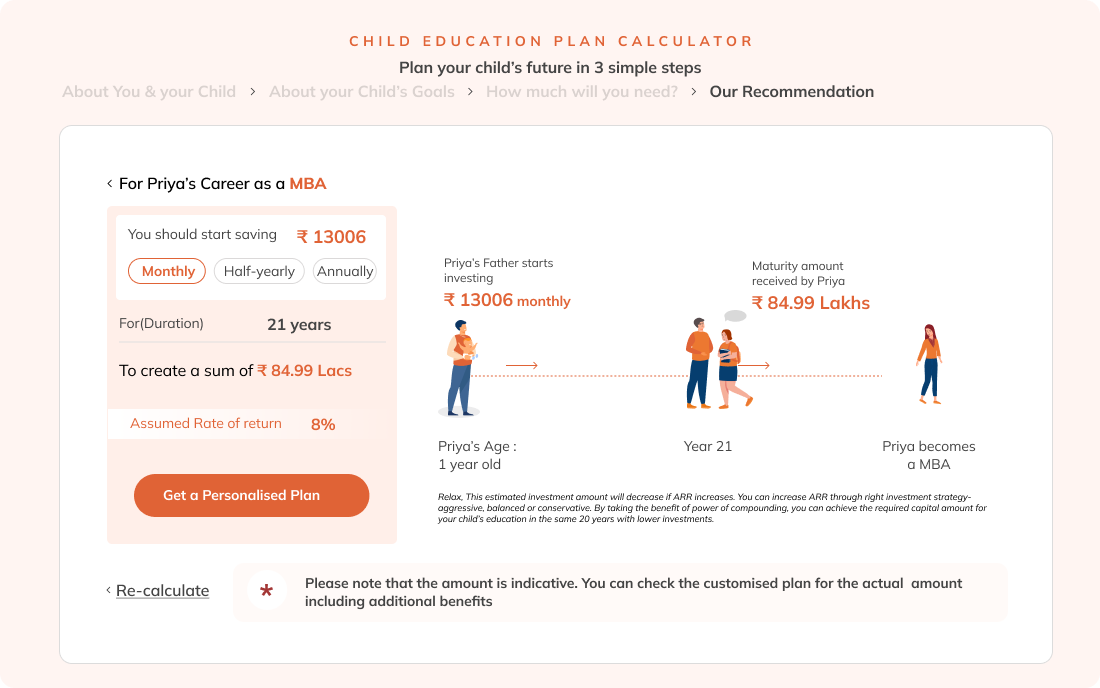

How much should you save for your child’s education?

When planning for your child's future education, it is important to account for factors like inflation. Education costs can rise over time.

For example, suppose your five-year-old child wants to become a lawyer. The approximate cost of pursuing a

law degree today may be around ₹8 lakh.

However, if your child is currently young and will begin college at age 21, the cost will increase due to

inflation.

Assuming an 8% annual inflation rate, ₹8 lakh today could grow to approximately ₹27.41 lakh by the year 2042. Hence, your

investment plan should aim to accumulate ₹27.41

lakh by the time your child turns 21. If you start saving now and have 16 years to invest, and your

investments generate an average return of 12% per annum, you would need to invest approximately ₹6,974 per month to reach this

goal.

Since every child’s goal and age may differ, you can use a child education calculator to

estimate the required corpus and monthly investment based on the expected inflation rate and your needs.

Factors to consider when planning for your child’s education

Below are some factors to consider when planning for your child’s education needs:

Education goals

Your planning should depend on your child's education goals and interests. Different courses have different costs. For example, professional degrees such as medicine or engineering may cost more. The location, whether in India or abroad, also impacts the total expense. Therefore, clearly identifying your child’s goals can help you plan more accurately.

Current financial status

Your current financial situation determines how much of your child’s expenses you can manage from your regular income and how much you need to save or invest. Based on your income and expenses, you can create a realistic budget that can help you reach your goals.

Right investment options

Your education savings goal can only be achieved with the right investment strategy. You must choose investment options that align with your time horizon and financial goals. It is equally important to consider your risk appetite before selecting the right investments.

Financial protection

Having life insurance secures the child in the unfortunate absence of the earning parent. You may consider combining an investment plan with adequate life cover1 for comprehensive security.

Timely plan adjustments

Regularly reviewing and adjusting your education plan is essential. Since inflation can impact education costs over the years, periodic reviews can help ensure that your savings and investments stay aligned with your goals.

Why is early planning for your child’s education important?

Here’s why early financial planning for your child’s education is important:

Long-term education goals

Early planning helps you prepare for your child’s long-term education goals. You have more time to invest in suitable instruments and grow your savings over the years. This reduces financial stress.

Rising education costs

Education costs increase over time due to inflation. Tuition fees and related expenses can be higher in the future. Planning early allows you to account for inflation and ensure that you accumulate the required corpus in time.

Financial preparedness

Early financial planning prepares you for future expenses. It ensures you have sufficient funds to cover your child’s education costs when the time comes, so you do not have to depend on loans.

Investment strategy

Starting early allows you to create a structured, goal-based investment strategy. With a longer time horizon, you can choose the right investment options and build a large corpus over time.

Child’s financial security

Early planning strengthens your child’s financial security. When combined with adequate life insurance, it ensures that your child’s education expenses can be covered even in your absence.

Flexible planning

When you begin early, you have the flexibility to review and adjust your investments over time. As your child’s goals evolve, you can modify your strategy to stay aligned with changing needs.

COMP/DOC/Mar/2026/183/2206

FAQ on Child Education Plan Calculator

What is Child education planning?

To give an understanding of how this can work out, do take a look at the below figures:

If as a parent you are looking to send your child abroad for higher education, the above costs can be considerably higher as well, depending on the country and university that you wish to send your child for further studies.

Why should I use a Child Education Planner to calculate future education costs?

Can the Child Education Planner be used for other financial goals, like planning for a child's marriage?

How accurate is the Child Education Planner in estimating education expenses?

Reference for CPI for education:

https://www.statista.com/statistics/655041/consumer-price-index-of-education-india/

https://www.thehindubusinessline.com/data-stories/data-focus/after-a-massive-dip-in-2021-education-inflation-rises-with-return-to-normalcy/article65513706.ece

https://www.moneycontrol.com/news/business/personal-finance/how-education-inflation-can-hurt-your-childs-future-8682261.html

`Reference for Average estimated cost of educational courses:

https://www.moneycontrol.com/news/business/personal-finance/childrens-day-how-to-save-for-your-kids-expensive-college-education-7711131.html

https://www.cnbctv18.com/india/how-your-child-can-still-make-it-to-the-dream-college-despite-rising-education-inflation-13816892.htm

https://collegedunia.com/courses/master-of-technology-mtech

https://www.aviationfly.com/how-much-is-the-commercial-pilot-training-cost-in-india/

https://collegedunia.com/courses/bachelor-of-arts-ba-journalism

COMP/DOC/Jul/2023/257/3597

COMP/DOC/Jun/2025/136/0484

COMP/DOC/Jan/2026/61/1784

COMP/DOC/Mar/2026/183/2206

BEWARE OF SPURIOUS / FRAUD PHONE CALLS!

IRDAI is not involved in activities like selling insurance policies, announcing bonus or investment of premiums. Public receiving such phone calls are requested to lodge a police complaint.