{kind=link}

Market Outlook

| June 30, 2026 | 1 Month |

1 Year |

|

| Rupees per Dollar | 94.67 | 95.00 | 85.54 |

| Oil (dollars per barrel) | 72.92 | 92.05 | 67.61 |

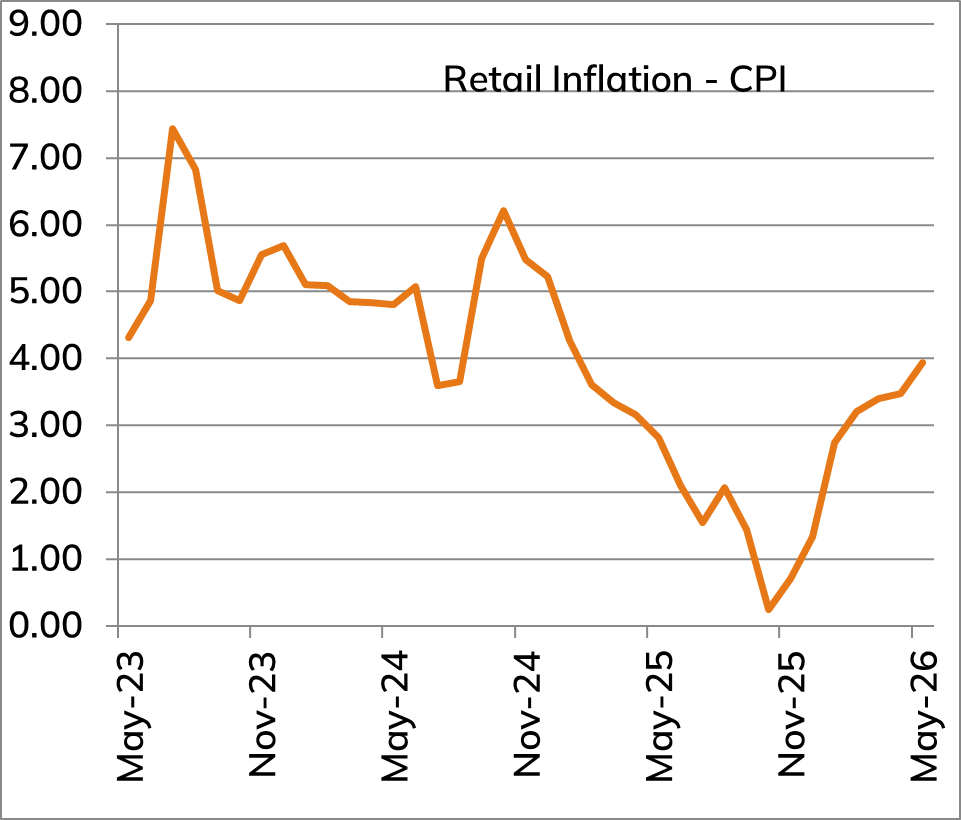

| Retail inflation (CPI) | 3.93% (May) | 3.48% | 3.03% |

- RBI kept the policy rates unchanged at 5.25% in June while announcing key measures to shore up capital flows. Measures like covering hedging costs on FCNR(B) deposit and concessional forex swap window for PSUs to hedge ECBs may lead to inflow of USD 70 – 90 billion.

- Easing of Geopolitical tensions has led to a sharp fall in crude prices. This has led to expectations of easing inflation thereby, reducing the pressure on Central banks to hike rates immediately.

- Removal of withholding tax on interest income and capital gains for FPIs and expansion of debt securities under Fully Accessible Route (FAR) has boosted sentiments on the back of probable inclusion of Indian Government bonds in Bloomberg Global Aggregate Index

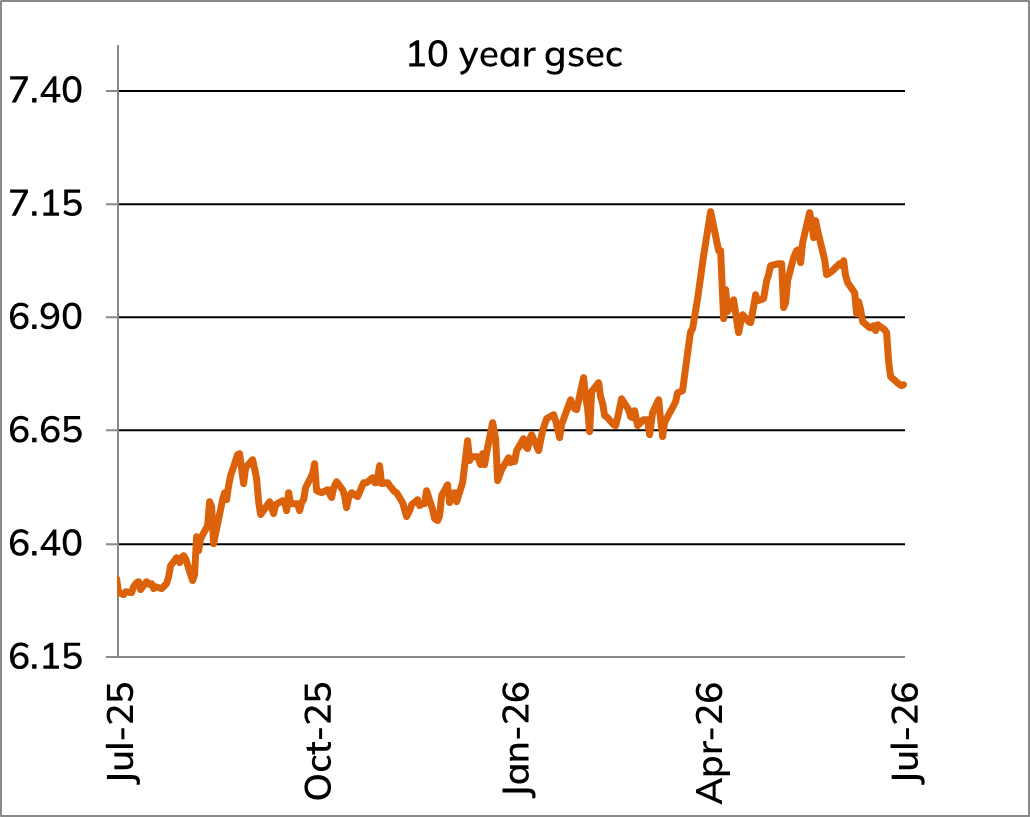

- All the above set of measures from RBI and Government along with fall in crude prices has helped Rupee to stabilize and 10Y benchmark yield to fall from 7.15 % to 6.75%. While we do not expect any immediate rate hike by RBI, we expect 10Y benchmark to trade in 6.60%-6.85% range.

| Index | 1 month (%) | 1 year (%) | 3 years (%) |

|---|---|---|---|

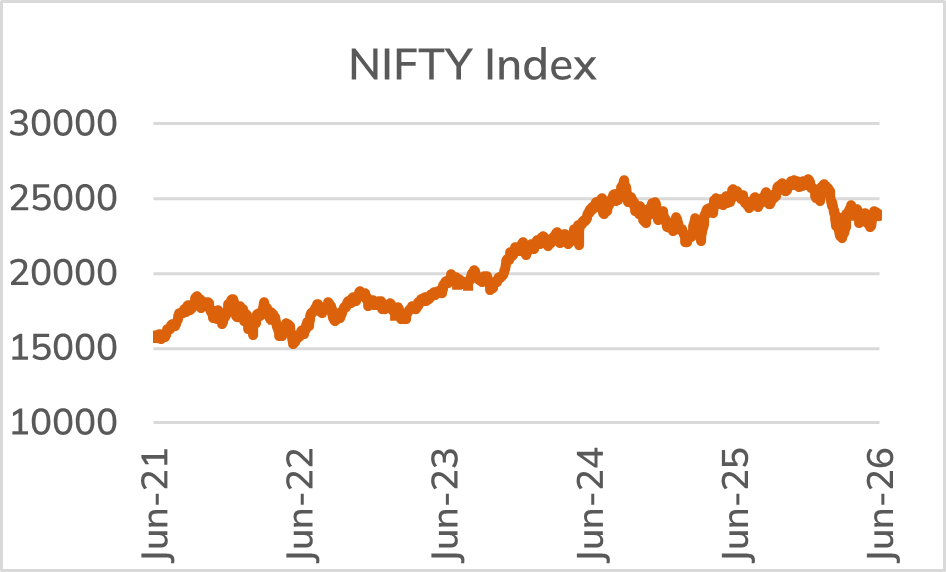

| NIFTY50 | 1.4 | -6.5 | 7.5 |

| BSE100 | 1.4 | -5.0 | 9.1 |

| NIFTY500 | 1.5 | -2.6 | 11.9 |

| NIFTY Midcap100 | 0.1 | 3.4 | 20.0 |

At June 30, 2026

Nifty was up 1.4% for the month of June 2026

- Easing geopolitical risk and reduced crude oil prices reversed market sentiment.

- Small cap indices out-performed mid and large cap indices. Within BSE 100 index, amongst sectors Retail / Banking outperformed while Technology / Metals & Minerals underperformed the broader market

We maintain our positive stance over the short as well as medium term

- US-Iran signed a MOU to end the war however situation needs to be monitored.

- FIIs selling seems to be moderating

- Weak southwest monsoon due to El Niño may impact growth outlook

- Nifty’s FY27 P/E is at 20x and is in line with 5-year average

Over the medium term, we expect following drivers for growth to play out:

- Fiscal and monetary policy support to continue to boost domestic demand

- Free Trade Agreements sealed with major economies/ economic blocs like the EU, the UK, Australia, New Zealand, Qatar etc. to support domestic economy. Potential deal with the US likely in the current fiscal.

- The government’s focus on building a resilient economy through energy security and policy reforms with the aim to enhance the business environment and attract foreign investment.

Market consensus for Nifty earnings CAGR over FY2026-28 at 15%

COMP/DOC/Jul/2026/57/0531