What is Life Insurance?

Life Insurance - Meaning

Life Insurance can be defined as a contract between an insurance policy holder and an insurance company, where the insurer promises to pay a sum of money in exchange for a premium, upon the death of an insured person or after a set period. Here, at ICICI Prudential Life Insurance, you pay premiums for a specific term and in return, we provide you with a Life Cover. This Life Cover secures your loved ones’ future by paying a lump sum amount in case of an unfortunate event. In some policies, you are paid an amount called Maturity Benefit at the end of the policy term.

There are two basic types of Life Insurance plans -

- 1. Pure Protection

- 2. Protection and Savings

What is Pure Protection Plan?

A Pure Protection plan is designed to secure your family’s future by providing a lump sum amount, in your absence.

What is Protection and Savings Plan?

A Protection and Savings plan is a financial tool that helps you plan for your long-term goals like purchasing a home, funding your children’s education, and more, while offering the benefits of a Life Cover.

Why do I need a life insurance policy?

Here’s why you need a life insurance policy:

Financial protection for your family:

A life insurance plan offers a payout to your family if something happens to you. This payout can help them with their essential expenses, outstanding loans and other financial needs.Support in case of health issues:

Life insurance offers financial support by waiving premiums in case of disability due to an accident. It also offers extended financial coverage in the case of critical or terminal illness, ensuring you have financial aid when you need it most.Tax benefits:

Life insurance premiums qualify for deductions subject to conditions prescribed under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4 )$ and payouts are exempt subject to conditions prescribed under Section 11 (read with Schedule II, Sr. No. 2)$ of the same act.Wealth creation:

Life insurance plans accumulate cash value, which allows you to build wealth over time while staying financially protected.

How to choose the right Life Insurance policy type?

Here’s what to consider when choosing the right life insurance policy:

Assess the policy features:

Review the plan’s details carefully to ensure it aligns with your life stage and financial objectives.Identify your financial priorities:

Evaluate your financial objectives. For instance, consider asking yourself whether you primarily need life protection to secure your family’s future or if you want to build wealth over time. You can then select a plan accordingly that meets your primary goal.Consider your budget:

Check the premium amount and ensure it fits within your budget.Evaluate riders and their costs:

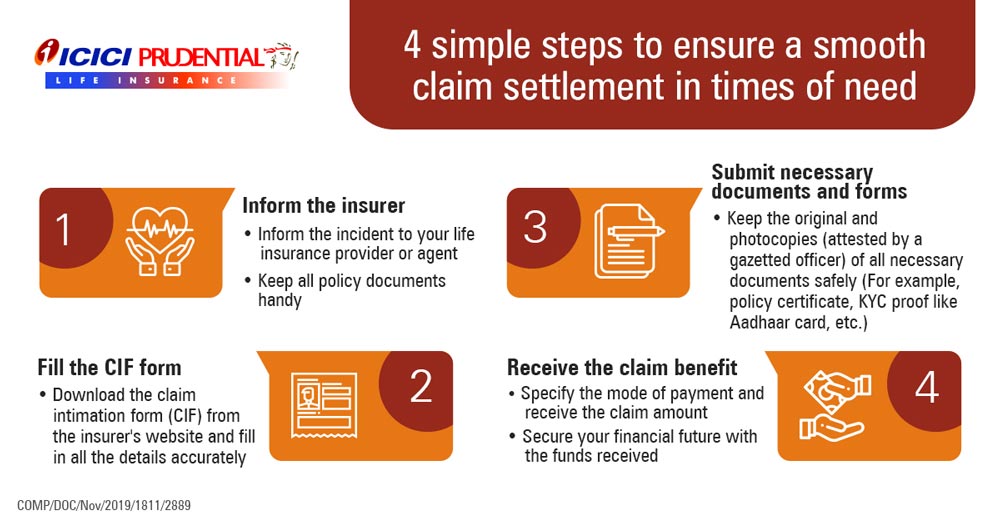

Look for optional add-on riders. These riders help to enhance the plan’s coverage based on your needs. Make sure your chosen plan offers the riders you need.Check the insurer’s claim settlement ratio:

Make sure to select a plan from an insurance company that has a higher claim settlement ratio. This ensures credibility of the insurer and better financial protection for your loved ones and offers you peace of mind.

COMP/DOC/Nov/2025/1711/1510

Factors that affect life insurance premium

Now that you know what is life insurance and why you need it, find out the factors that can affect the life insurance premium:

Age:

One of the prime factors that affect the premium for a life insurance plan is your age. The life insurance premium is lower for younger people and gradually increases with age.Gender:

Studies have shown women live longer than men1. Therefore, the life insurance premium is lower for women as compared to men.Health conditions:

Your present and past health conditions can determine the premium for your life insurance plan. If you have any pre-existing illnesses or have suffered from an illness in the past that may resurface or affect your present health, you would be charged a higher premium.Family health history:

The chances of suffering from a disease that runs in your family are considerably high. So, if any hereditary illnesses run in your family, you may have to pay a higher premium.Smoking and drinking alcohol:

Lifestyle habits like smoking and drinking alcohol can impact your health and lead to multiple health issues. Therefore, insurance companies charge a high premium for individuals who smoke or drink alcohol.Type of coverage:

The type of coverage you opt for can increase or decrease the life insurance plan’s premium. If you add any riders to your plan, the premium would increase. A longer policy term can also result in a higher premium compared to a shorter term. In addition to this, the type of life insurance plan you select also impacts the premium. For instance, term life insurance is the most affordable form of life insurance.Amount of coverage:

A higher sum assured would result in a higher premium and vice versa.Occupation:

If you work in a high-risk job, the premium for your life insurance plan would be higher than others. For example, if you work in construction or if your job puts you at any kind of risk, such as regular exposure to chemicals, the insurance company will charge a higher premium.

COMP/DOC/Dec/2021/3112/7177

What are the benefits of having Life Insurance?

Life insurance can offer several benefits to you and your loved ones, including the following:

Financial Security

Wealth Creation

Tax benefits

When you buy a life insurance policy, the insurance company charges a premium in exchange for providing financial security to your beneficiaries in case of an unfortunate event of death. The proceeds from life insurance can be used by the beneficiaries as an income replacement to cover day-to-day expenses.

Some life insurance plans offer you the option to invest and grow your money. This enables you to stay financially prepared for your future needs. Life insurance can offer good returns and income.

Life insurance plans offer multiple tax$ benefits. The premiums paid towards a life insurance plan are deductible up to ₹ 1.5 lakh per annum under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4 )$ and the maturity benefits are also tax-free subject to conditions prescribed under Section 11 (read with Schedule II, Sr. No. 2)$ of The Income Tax Act, 2025.

COMP/DOC/Apr/2023/104/2751

Let us understand some commonly used terms in Life Insurance:

- Life Assured: It is the person who is covered under the insurance policy.

- Proposer: It is the person who pays the premiums of the policy. For example: If you have bought the policy for yourself, then you are both the Life Assured as well as the Proposer. Similarly, if you purchase an insurance policy for a family member, then you are the proposer and the family member is the Life Assured.

- Nominee or Beneficiary: It is the person you appoint at the time of buying the policy to receive the benefits of your insurance policy, in your absence.

- Insurer: The insurance company that sells the life insurance policy is called the Insurer (for example, ICICI Prudential Life Insurance).

- Life Cover: It is the amount that the Insurer will pay to your Nominee in case of an unfortunate event.

- Maturity Benefit: For Protection + Savings policies, the Insurer pays a certain lump sum of money on completion of the policy term. This amount is known as the Maturity Amount.

- Premium: A premium is the amount you pay to the insurer for receiving the benefits of the insurance policy. These payments can be made on a regular basis throughout the policy duration, for a limited number of years or just once, as per the options available under the policy you choose.

- Premium Payment Term: The number of years for which you pay the premiums is known as the Premium Payment Term.

- Policy Term: The number of years for which the Life Cover continues.

Let us understand how Life Insurance works:

In today's era, having a life insurance policy is a must for every individual as it is one of the best ways to secure one's future along with their loved ones. There are many different types of life insurance policies available in the market. However, before choosing one, it is important to understand how a life insurance policy works. Let us look at an example to understand how life insurance works:

Now, let’s see an example:

Mr. Kumar (Life Assured) pays ICICI Prudential Life Insurance (Insurer) an annual amount (Premium) over 5 years (Premium Payment Term) to make sure that his wife (Nominee) gets a certain assured sum of money (Life Cover) in case of an unfortunate event during the 10 years or Lumpsum amount at maturity on survival at the end of policy term.

Life insurance not only covers the risk arising due to an unfortunate event, but also gives you additional benefits like tax benefits, savings and wealth creation over a period of time. The right life insurance from a trusted company can help one get long-term risk cover plus savings, i.e. dual benefits from one solution.

COMP/DOC/Sep/2021/249/66267

People like you also read ...

{kind=link}