IN ULIPS, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICYHOLDERU

The Linked Insurance Products do not offer any liquidity during the first five years of the contract. The policyholder will not be able to surrender or withdraw the monies invested in Linked Insurance Products completely or partially till the end of the fifth year.

As a parent, you want to provide the best future for your children. This can be quite a demanding task with the rising inflation and changing lifestyle. Most items and objects that are associated with your daily life have continued to become more and more expensive over the years including housing, fuel, clothing and common foods like pulses, vegetables and eggs.

The rising cost of inflation may make it very tough for the coming generations to manage the varied demands of their lifestyles. However, you have the opportunity right now to work towards making it easier for your children in the future. By planning in advance and investing your money smartly, you can indeed secure your children’s future and help them fulfil their dreams.

What are child savings plans?

Child savings plans are insurance plans that can help you save for your child’s future expenses, such as education, marriage, extracurricular activities and other financial needs. These plans combine a savings component with life insurance to ensure that your child’s financial future is protected even in your absence.

Why is saving for your children important?

Here are some reasons why saving for your children is important:

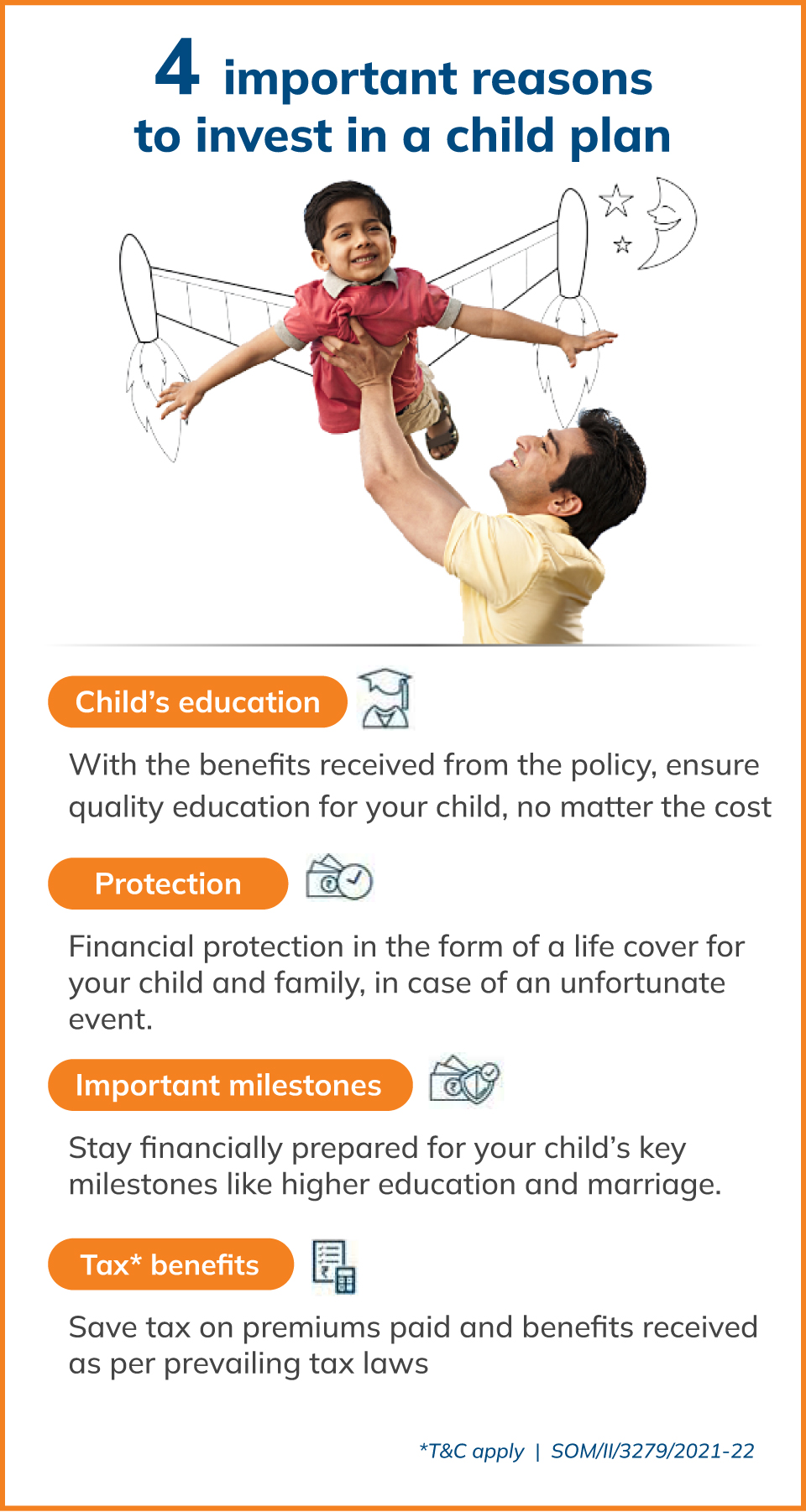

Birth of a child

Financial planning helps you prepare for the birth of a child. Having a child can come with several costs, including delivery expenses, regular checkups, vaccinations and more. Saving for these expenses ensures that you can focus on the joy of welcoming your child instead of worrying about the financial burden.

Education

Saving for your child ensures that you have adequate funds to cover their education expenses. Schooling can involve several costs such as uniforms, tuition fees, books, computers and more. Financial planning helps you take care of all such expenses.

Higher education

Financial planning ensures you are prepared for higher education expenses like college. It also helps you account for inflation and prepare for costs related to studying abroad, professional courses and specialised programs.

Marriage planning

Saving for your child allows you to manage wedding expenses more comfortably and helps you support them as they begin a new phase of life.

Emergency needs

Financial planning allows you to be prepared for unexpected expenses and ensures that your family remains financially secure during emergencies.

How do child savings plans work?

Start saving early

Saving in a children savings plan early helps you build a large corpus. You can start small and build wealth over time through compounding. Beginning early also allows you to spread your savings over a longer period.

Regular contributions

Paying the premium regularly helps you develop consistent financial habits and grow wealth steadily over time. It also ensures that your policy remains active while helping you build long-term financial security for your child.

Long-term wealth creation

Saving regularly in child savings plans helps you build long-term wealth. This can help you achieve major financial goals for your child, such as higher education, marriage and other future needs.

Goal-based payout

Saving in a child savings plan can help you achieve several financial goals. These plans often offer payouts that align with specific life milestones such as education, marriage or other important events, and ensure financial support when it is needed the most.

Financial protection for the child

A child savings plan ensures financial security for your child's future needs, even in the absence of a parent. The life cover1 helps protect the child's financial future and ensures their goals can be achieved.

What are the best child savings plans in India in 2026?

Below are some of the best savings plans for a child in India in 2026:

Child Unit Linked Insurance Plans (ULIPs)

Refer policy document for T&C

Child ULIPs combine market-linked investments with the security of life insurance. They are designed to help you build wealth for your child’s future goals. Even if you are not around, the plan continues to offer financial protection. Plus, you get tax* advantages under Sections 123 (read with Schedule XV, Sr. No. 1, 2 & 4), and 11 (read with Schedule II, Sr. No. 2) of The Income Tax Act, 2025.

Child education insurance plans

Child education insurance plans are specially crafted to help you financially prepare for your child’s education costs. These plans are tailored to account for education inflation, so you can build a fund for your child’s academic needs. Along with investment growth, they also offer life cover that ensures your child’s education is not compromised even if you are no longer around. These plans also come with tax* benefits under Sections 123 (read with Schedule XV, Sr. No. 1, 2 & 4), and 11 (read with Schedule II, Sr. No. 2) of The Income Tax Act, 2025.

Life insurance plans

Life insurance plans are a protective financial tool for your child’s future. In the unfortunate event of your absence, these plans ensure that your child is financially secure and supported.

Systematic Investment Plan (SIP)

A SIP allows you to invest a fixed amount of money in mutual funds at regular intervals. You can select from equity, debt or hybrid funds, as per your risk-taking ability comfort with risk and your long-term financial goals. SIPs can be an effective way to fund your child’s school and college education, international studies and other needs.

Sukanya Samriddhi Yojna (SSY)

The SSY is a government-supported savings plan designed exclusively for girl children below the age of 10. You can start investing with as little as ₹ 250, while the annual deposit limit goes up to ₹ 1.5 lakh. Not only are the contributions eligible for deductions under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4), but the interest earned is also exempt from tax* under Section 11 (read with Schedule II, Sr. No. 2) of The Income Tax Act, 2025.

Debt funds

Debt funds are mutual funds that invest in debt or fixed-income instruments like bonds, government securities and others. They carry lower risk compared to equity funds, making them ideal for conservative investors. You can start investing in them through SIPs or make a one-time lump sum investment. Debt funds come in 16 types to suit different investment horizons and risk levels, including Liquid Funds, Ultra Short Duration Funds, Short Duration Funds, Dynamic Bonds, Gilt Funds and others.

Public Provident Fund (PPF)

PPF is a long-term, government-backed savings scheme that offers a fixed interest rate compounded annually. With a lock-in period of 15 years, PPF is ideal for long-term goals. PPF contributions qualify for deductions under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4), and both the interest earned, and the maturity amount are tax-free* under Section 11 (read with Schedule II, Sr. No. 2) of The Income Tax Act, 2025.

Gold

Gold is a smart hedge against inflation and market volatility. You can invest in it in different forms, including traditional jewellery, physical gold like bars and coins, market-linked Gold Exchange Traded Funds (ETFs) and gold mutual funds. Gold can help you diversify your portfolio, while offering steady returns through appreciation.

National Savings Certificate (NSC)

NSC is a fixed-income investment backed by the Government of India. You can purchase NSCs from any post office. With a five-year lock-in period, the scheme offers compounded annual interest and deductions of up to ₹ 1.5 lakh under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4) of The Income Tax Act, 2025. NSC is designed for low-risk, dependable returns.

What are the key factors to keep in mind when choosing a child savings plan?

When choosing a children savings plan, consider your purpose, plan’s investment duration, flexibility, and potential returns, as well as tax benefits and the insurers’ reputation. Ultimately you should ensure that the plan aligns with your goals and meets both short-term needs and long-term objectives.

Purpose of the plan

Knowing the specific purpose of a child saving plan is essential, as it helps tailor the plan to meet your child's unique future needs. For example, you could save for your child's higher education, healthcare, or to support a significant life event like marriage. For instance, if your priority is higher education, a plan that offers higher returns and aligns with the college timelines may be ideal. On the other hand, if you are focused on healthcare or other emergency needs, a plan with liquidity options for early withdrawals might be better suited. By defining the purpose early on, you ensure that every contribution moves you closer to fulfilling your child's dreams and future milestones.

Evaluating the plan's duration

The duration of a child saving plan plays a vital role in building your child's future. A longer investment horizon will let your funds have more time to compound and accumulate. For instance, starting a savings plan when your child is young enables the fund to grow significantly by the time they are ready for higher education or other milestones. Therefore, choosing a plan with an appropriate time frame ensures that savings align well with future needs.

Ensuring flexibility

Flexibility is a valuable feature in a children savings plan, as it allows parents to adjust their contributions, make withdrawals, or switch funds as life circumstances change. A flexible plan lets you modify the amount you invest over time, so you can increase contributions during prosperous periods or reduce them if other financial obligations arise. Additionally, some plans offer partial withdrawal options, allowing you to access funds in case of an emergency without compromising the overall savings goal. For parents considering market-linked options, the ability to switch funds ensures that you can adapt your investment strategy to changing market conditions. Ultimately, a flexible plan provides peace of mind by offering both stability and adaptability as your family's needs evolve.

Returns and performance

Evaluating a child saving plan's historical returns and performance helps ensure that your investment will meet future financial needs. Reviewing a plan's past performance can give insight into its growth potential. Comparing returns over the last 5–10 years is a good way to gauge how well a plan has fared through varying market conditions. By choosing a plan with a strong track record, parents can confidently invest in the best saving plan for their child that balances both growth and stability.

Understanding tax benefits

Tax benefits play an important role when choosing a children savings plan, as they can reduce your overall tax liability and enhance savings. Many child saving plans offer deductions under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4)~ of the Income Tax Act, allowing parents to claim up to ₹1.5 lakh in deductions annually on the premiums paid. Additionally, plans that qualify under Section 11 (read with Schedule II, Sr. No. 2)~ provide tax-free maturity benefits, which means the payout at the end of the policy term is exempt from tax, provided certain conditions are met. By choosing a tax-efficient plan, you not only secure your child's future but also maximise your own tax savings, making it a win-win investment for both short-term relief and long-term growth.

Reputation of the provider

Choosing a reliable and reputable insurer is vital when selecting a child saving plan. An insurers reputation can directly impact the security and performance of your investment. You can assess the claim settlement ratios, customer service quality, responsiveness and years of experience in the industry. Opting for a trusted institution helps ensure that your child's future is in safe hands and that any potential claims will be handled smoothly.

Inflation

Inflation significantly impacts the future value of savings in a child saving plan. As the cost of education (11-12% p.a.)@, healthcare (14% p.a.)&, and living expenses (5-6% p.a.)( rise over time, the purchasing power of today's savings may diminish, affecting your ability to meet future financial goals. For example, an amount that seems sufficient for a college education today may fall short years later due to inflation. Choosing a plan that offers returns capable of outpacing inflation can help counter this effect. By accounting for inflation, you ensure that your savings will retain their value, supporting your child's aspirations even as costs increase over time.

Exploring automatic features

Automatic features like auto-debit and fund rebalancing add convenience and reliability to a children savings plan fostering disciplined investment and ensuring consistent progress towards long term goals.

Consultation

Seeking professional financial consultation can offer personalised guidance based on your unique goals, budget, and risk tolerance, helping you select the best saving plan for your child. With insights into market trends, tax benefits, and inflation impacts, an advisor can ensure that your choice aligns with both your immediate and long-term needs.

How do savings plans for children help secure your child's future?

There are several benefits of children savings plans, such as:

The dual advantage of savings and life cover1

These plans offer the dual benefit of savings and life insurance. They help you save for your children’s future and, at the same time, ensure their financial security in case of an unfortunate event.

Emergency funds

These plans can be used in case of a financial emergency. They let you make partial withdrawals that you can use for any immediate needs.

Financial security

In case of an unfortunate event, savings plans for children provide a lump sum payment in the form of the claim amount. Additionally, the plan continues to be active and the life insurance company takes care of all future premium payments. The payout received at the end of the policy term ensures that your children’s dreams are fulfilled, no matter what.

Tax~ benefits

These plans also offer tax benefits on the premiums paid up to ₹ 1.5 lakh in a financial year under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4) . The payout received at the end of the policy term is also tax-exempt~ under Section 11 (read with Schedule II, Sr. No. 2) of the Income Tax Act, 2025.

Focus on long-term savings

With a child saving plan, long-term investments can grow significantly through compounding, allowing your money to earn returns on both the initial contributions and the accumulated interest over time. A steady, long-term approach ensures that by the time your child reaches important milestones—such as higher education or marriage—there is a substantial fund available to support their dreams.

Securing guaranteed returns

A child saving plan with guaranteed` returns provides parents with a sense of security and predictability. Plans that offer guaranteed` returns ensure that, regardless of market fluctuations, you will receive a fixed maturity amount. This certainty allows parents to plan confidently for future expenses like education or marriage, knowing exactly how much they will have when needed.

Stay consistent

Child savings plans help you stay consistent with regular savings. They keep you financially disciplined and ensure that you remain on track with your long-term goals while protecting your child's financial future.

Check for extra benefits

Additional features, such as riders, can enhance the coverage of the plan and provide extra financial protection in adverse situations. These benefits can offer more comprehensive security for your family.

`Terms and conditions apply

COMP/DOC/Jan/2025/271/8210

Why should you start saving for your children at an early age?

Here's why you should start saving for your children at an early age:

Benefit of early savings

Starting early helps you build a larger corpus through the power of compounding. It boosts your savings over time and helps you reach your financial goals more comfortably than if you start later. Early investing also allows your money more time to grow, which makes it easier to meet your target amount.

Lower financial stress later

Early financial planning helps reduce financial stress in the future. It prepares you for major expenses and allows you to manage your needs without financial pressure.

What are the major milestones to focus on when choosing a child savings scheme?

There will be many important milestones in your children’s lives that you need to plan and save for. These include:

School education

School fees are a major expense that one needs to account for. Although the fees of top schools can often be quite expensive, it is every parent’s top priority to get their children admitted to the best. Ultimately, good schooling is instrumental in preparing your children for a successful future. So, you must invest in it as much as you can.

Higher education

Higher education can be quite expensive in our country#. Specialist courses like engineering and medical science often have higher fees. Moreover, many children nowadays are choosing more off-beat career options like music or other performance arts.

Since this is a relatively new trend in India, there aren’t many colleges that can match the expertise and infrastructure provided by colleges abroad. If your children decide to opt for such a course, you may have to send them overseas for further education sooner or later. As a parent, you need to support your children’s choices and passions, and having a financial plan will enable you to do just that.

Marriage

Marriage is one of the most important milestones in a person’s life. Your children might decide to get married early in life when they have just started their careers. At this stage, they might require your assistance in taking care of their marriage expenses. Even if they decide to get married at a later stage, every parent wishes to support their children emotionally and financially as they start a new chapter of their life. Ultimately, a child’s marriage is a very special occasion for any parent and you want to celebrate it in the best possible way without sparing any expenses or making any compromises. That is why it is important to plan and save for your children’s marriage.

What are the best tips for saving money for your children’s future?

Start early

The sooner you begin, the more you can save. A longer term helps to earn better returns. Starting early also means that you can save smaller amounts regularly, which also makes it easier on your pocket

Be regular

Always deposit amounts as and when you can, instead of waiting until you have a large amount. Saving regularly also helps you to accumulate money that can support your children’s dreams

Look for added benefits

When opting for a life insurance plan, look for a plan that offers added benefits, in the form of bonuses. This will enhance your overall earnings

Don’t exceed your budget

The amount that you decide to save for your children should fit comfortably within your budget. If you exceed your budget, you might either end up compromising on your present needs, or find it difficult to keep saving regularly

COMP/DOC/Jan/2022/111/7229

People like you also read ...

{kind=link}