Benefits of Life Insurance

What is Life Insurance and how is it helpful?

Life insurance offers many benefits, which is why is it considered to be one of the most important financial tools for an individual. It gives you a chance to build wealth and provides your loved ones with financial security in your absence. Life insurance also offers you different opportunities to invest while taking care of your retirement needs.

Read on to know more benefits of life insurance:

- Term Insurance: Term insurance plans provide life cover to protect your loved ones at most affordable rates. This is the simplest form of life insurance. Term plans offer financial security to your loved ones’ future even in your absence.

- ULIP: Unit linked insurance plans, better known as ULIPs, combines life insurance with financial investment. Unit-linked insurance plans offer a wide choice of fund options and portfolio strategies. ULIPs allow you to withdraw money regularly from your policy after 5 years lock-in.

- Endowment Plan: Traditional savings insurance plans are risk-free investment plans that also offer insurance shield. Better known as endowment and money back policies, traditional plan returns are not linked to the stock market, and hence carry lower risk. Traditional insurance plans offer bonus, such as reversionary bonus and terminal bonus, for staying invested, which enhances the maturity sum.

- Savings Plan: Savings Plans are life insurance plans that combine the benefits of a life insurance cover and investment. So, in addition to securing yourself and your family, you also create a corpus to meet your financial goals at every life stage. Most protection and savings plans usually offer you a fixed amount as Maturity Benefit when the policy ends, but some specific plans also help you create a regular stream of income throughout your policy duration

- Whole Life Insurance Plan: Whole Life Insurance Plan cover you up till 99 years of age. They are different from ordinary insurance policies which have a defined term of say 10, 20 or 30 years, and are of use when you have financial dependents for a relatively long period, possibly your entire life.

- Retirement and Pension Plan: Retirement insurance plans offer ways to build your own pension income. You can either choose to accumulate your retirement corpus as per your risk appetite, or get guaranteed immediate income for life by investing a lump sum.

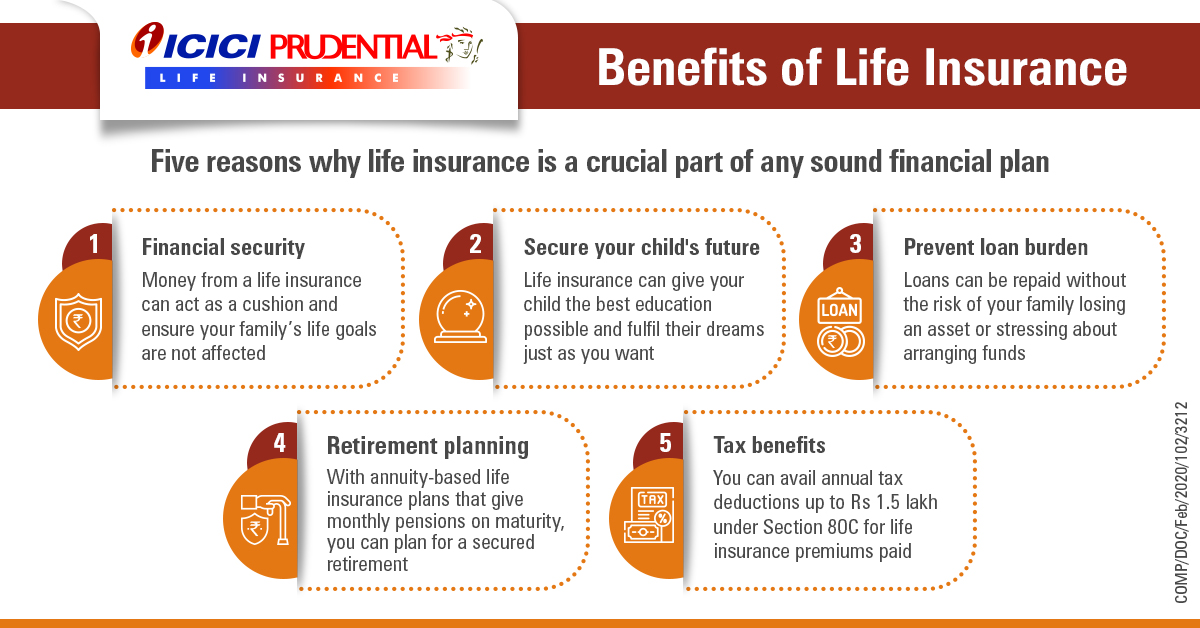

Why life insurance is a crucial part of any sound financial plan?

What are the benefits of having Life Insurance?

The various benefits of having life insurance are as follows:

- Peace of Mind/ Financial Security - Having life insurance provides the ultimate peace of mind. This is because if someone were to meet with their demise, they know their family and loved ones will have a financial safety net. All of us have some financial liabilities, but an adequate life insurance cover ensures that your debts or loved ones will be financially taken care of in the event of your death

- Wealth Creation - Some life insurance plans also offer you the opportunity to create wealth. Apart from life cover, these policies invest your premium in different investment classes to deliver superior risk-adjusted returns that beat inflation and grow your corpus.

- Tax Savings - Life insurance plans offer dual tax benefits^. The premiums paid offer tax deduction under Section 123 (read with Schedule XV, Sr. No. 1, 2 & 4 ) of the Income Tax Act. This means up to ₹ 1.5 lakh premium paid annually is deducted from your gross income, thus lowering your tax outgo. Separately, the maturity insurance plans may be entirely tax-free. This tax benefit^ is under Section 11 (read with Schedule II, Sr. No. 2) of the Income Tax Act

- Buy Young, Save More - Life insurance plans give you the ability to lock in low premium rates while you’re young. If you buy the same policy when you are older, you will be paying a much higher premium compared to if you bought the same plan when you were younger.

- Death benefit - In the unfortunate event of the demise of the policyholder, the policy’s nominee receives the entire sum assured amount as long as the premiums have been paid in full.The sum received from the term insurance can be used by the nominee for any reason to cover a variety of expenses ranging from clearing routine bills to paying back loans, paying for children’s fees or other expenses.

How are life insurance plans suitable for your needs?

Life insurance fills financial gaps that exist in your lives. As an all-rounder product, life insurance can take care of your different financial needs at different stages of life. All you have to do is identify the need, and there is a suitable life insurance plan for you.

- Saving for children’s education - A majority of Indians fund their children’s education. On an average Indian parents spend over ₹ 12 lakh on children’s education. Thus, saving for a child's education is one of the biggest priorities for a parent.

Child insurance plans allow you to fulfil this financial need. Such policies, often in the form of a Unit Linked Insurance Plan, help grow your investments and help you secure the educational milestones of your children.

- Financial Protection in case of major illnesses/health issues - A majority of Indians spend around 70% of their income on medicines and health care. Down with a health issue such as major/critical illness, there is a high chance you will not be able to earn income during the treatment/recuperation period. But your family's financial needs will remain even if you are sick. Life insurance plans can provide financial protection during major illnesses.

Critical illness cover provides a lump sum payout on the diagnosis of a wide range of serious health related conditions. This lump sum payout is given on diagnosis only. Hence, there is no need to submit bills and patiently wait for claims after undergoing treatment. Critical illness plans give you money that you can spend on your treatment, and fund your household during your no-income period as you undergo treatment. There is no restriction on how you use the claim money.

- Retirement planning - Retirement is supposed to be this beautiful time when you are free from work pressures and life is peaceful. It can be all those things and much more, if you have a pension/monthly income. Most of us work in private sector companies, and hence there is no pension benefit. This is why retirement becomes more of a worry than something to look forward to. Fortunately, life insurance provides retirement plans that allow you to earn a pension, keep your head high and live your life in your own terms.

Retirement plans offer you and your spouse the benefit of receiving regular pension for life. If you start saving for retirement from an early age, saving a big retirement corpus is possible with a retirement plan. For that, consider your post-retirement financial requirements to build an adequate retirement kitty that will suit your old-age needs. With proper planning and saving through a retirement plan, you will be able to build a good retirement corpus, which can be used to buy a fixed pension plan for life and thus protecting yourself from inflation.

People like you also read ...

{kind=link}