Why is ICICI Pru Smart Life special?

You can enjoy the opportunity to get potentially better returns and grow your money by investing in equity and debt funds for the long term. This combination helps you beat inflation while protecting your investments.

How does a mix of equity and debt beat inflation?

Inflation is the rate at which the price of goods and services increases over a period of time. For example, the price of a particular item has increased from `100 in 2005 to `243 in 2017.

To gain from your investments, your savings should grow at a rate higher than the inflation rate.

In order to get better returns in the long run, it is advisable to have equity exposure. Equity markets are subject to short-term market volatility. However, the effect of market volatility is negligible in the long term.

Below is an example of how investing in a mix of equity and debt can help in building your savings,

If 60% of your money was invested in the equity market and 40% in debt market## in the last 12 years, your investment would have grown by around 12% on an annualized basis. This growth would have helped you stay ahead of the inflation rate of about 7.7%# in the same period.

#Source: CEIC, CSO, CPI inflation average of 12 years (from March 2006 to March 2017)

##Equity market: BSE 100; Debt market: CRISIL Composite Bond Index (from March 2005 to March 2017)

You may want to manage your investments yourself, or want an expert to do it for you. ICICI Pru Smart Life brings the best of both worlds. With the Fixed Portfolio Strategy, you can manage your money by investing it according to your risk appetite in equity and debt funds. On the other hand, with the Lifecycle-based Portfolio Strategy, we carefully manage your investments to create an ideal balance between equity and debt funds depending on your age.

Which portfolio strategy suits me the best ?

Fixed Portfolio Strategy: With this option, you can invest your money in equity and debt funds of your choice. You can also move your money from one fund to another to suit your investment needs.

Lifecycle-based Portfolio Strategy:With this option, your money is automatically allocated to equity and debt funds based on your age. As you grow older, your money is systematically transferred from equity to debt to secure it when the policy matures.

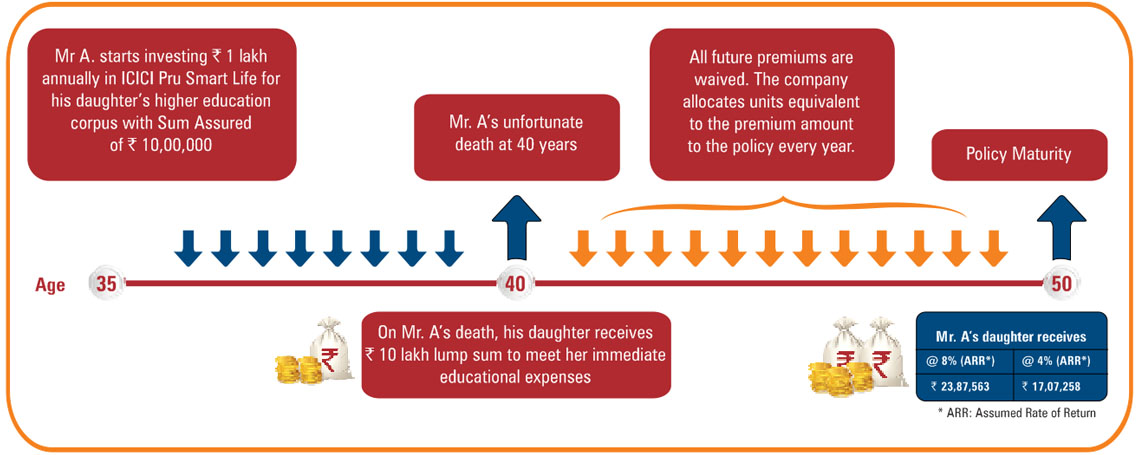

ICICI Pru Smart Life provides a life cover for you and your family’s all-round protection. In case of an unfortunate event during the policy term, your family receives a lump sum amount. This amount will help your loved ones live the life you planned for them.

How much money will my family receive in my absence?

In case of unfortunate demise of the person insured, the company pays in two ways:

a) Lump Sum Benefit – A lump sum benefit is paid out by the company to take care of any immediate liabilities of the family.

The Lump Sum benefit is the higher of the two amounts:

A fixed amount called the Sum Assured, including Top-up Sum Assured if any

Minimum Life Cover that is equal to 105% of the total premiums including Top-up premiums, if any received up to the date of death.

b) Smart Benefit – This benefit ensures that your savings continue to grow to fulfill your family’s goals. In case of an unfortunate event, the company pays the future premiums on your behalf and the policy continues uninterrupted.

How does the Smart Benefit work?

The company pays the premium in the form of units on the due date. On maturity of the policy, the nominee receives a lump sum of the Fund Value* including the Top-up** Fund Value, if any.

Smart Benefit is valid for regular premium policies and applies only if all due premiums have been paid.

*Fund Value is the total value of your money that is invested in equity and debt fund of your choice.

**Top-up is any extra amount that you can invest and add to your Fund Value.

To reward you for being a loyal customer, the company adds to your savings further with Loyalty Additions, which helps your wealth grow without the need for you to invest more money.

What are Loyalty Additions?

Loyalty Additions will be added as extra units at the end of each policy year, sixth policy year onwards. Each Loyalty Addition will be equal to 0.25% of the average Fund Values*. It includes Top-up** Fund Value, if any.

An extra Loyalty Addition of 0.25% will be paid every year after the 6th year if all premiums for that year have been paid. These Loyalty Additions will be allocated to your fund in the form of units. Loyalty Additions and Wealth Boosters will be equal to the above percentage of the average of the Fund Values on the last business day of the last eight policy quarters.

*Average of the Fund Values on the last business day of the last eight policy quarters where Fund Value is the total value of your money that is invested in equity and debt fund of your choice.

**Top-up is any extra amount that you can invest and add to your Fund Value.

The company also adds Wealth Boosters to your savings. This helps you grow your money without having to make any additional investments.

What is the value of Wealth Boosters that I will get?

Each Wealth Booster addition will be equal to 3.25% of the Fund Value average* in the Regular and Limited Pay options and 1.5% in One Pay option^. This will also include additional Fund Value from Top-ups**, if any. The additions are made once in 5 years starting from the end of the 10th policy year, which means for a policy term of 25 years, Wealth Boosters will be allocated four times.

Loyalty Additions and Wealth Boosters will be equal to the above percentage of the average Fund Values on the last business day of the last eight policy quarters.

^You can choose the number of years for which you wish to pay premiums. You can opt for either the One Pay option (One time lump sum premium payment) or the Regular Pay option (Regular payment of premiums throughout the policy term).

To know more about the minimum premium for all three options, please refer to the ‘Product at a glance’ section.

Is Wealth Booster a guaranteed feature of the product?

Yes, the allocation of Wealth Booster units is guaranteed and is subject to regular payment of premiums.

*Average of the Fund Values on the last business day of the last eight policy quarters where Fund Value is the total value of your money that is invested in equity and debt fund of your choice.

**Top-up is any extra amount that you can invest and add to your Fund Value.

Starting from the sixth policy year, you can withdraw a part of your money as per your need. This ensures that you have easy access to your money while at the same time, the rest of your invested money keeps growing.

How much money can I withdraw?

You can withdraw up to 20% of your Fund Value* at any time+ from the sixth policy year.

Am I charged for making partial withdrawals?

No, partial withdrawals are completely free of cost.

*Fund Value is the total value of your money that is invested in equity and debt fund of your choice.

+Provided monies are not in DP Fund. You can make unlimited number of partial withdrawals as long as the total amount of partial withdrawals in a year does not exceed 20% of the Fund Value in a policy year. DP Funds refer to Discontinued Policy Funds and consist of money from lapsed policy.

With this plan, you can reduce your taxable income by investing up to `1.5 lakh under Section 80C. This will help you save tax. What’s more, even shifting your money from equity to debt or debt to equity is completely tax-free*. The money you get at the time of maturity is also tax-free*

*Tax benefits under the policy are subject to conditions under Section 80C, 10(10D) and other provisions of the Income Tax Act, 1961. Applicable taxes will be charged extra as per prevailing rates. Tax laws are subject to amendments from time to time.

{kind=link}